EMIR Changes

Corporates, smaller financial counterparties and pension scheme arrangements (“PSAs”) stand to benefit if the European Commission’s recent proposal to amend EMIR1 is adopted. The proposed Regulation sets out a number of targeted modifications of EMIR, which are designed to eliminate disproportionate costs and burdens and to simplify the rules.These modifications relate in particular to the EMIR requirements on clearing, risk mitigation and reporting.

Overview of EMIR

EMIR imposes three main obligations on certain derivatives markets participants, namely:

- to clear certain OTC derivatives through a central counterparty (“CCP”) (the “Clearing Requirement”);

- to put in place certain risk mitigation procedures for uncleared OTC derivatives transactions (the “Risk Mitigation Requirement”); and

- to report derivatives to a trade repository (the “Reporting Requirement”).

EMIR also contains authorisation and supervision requirements applicable to CCPs and trade repositories.

EMIR applies to any entity established in an EU member state that enters into a derivative, including banks, insurance companies, pension funds, investment firms, corporates, funds and special purpose vehicles, subject to certain very limited exceptions. The Clearing Requirement and the Risk Mitigation Requirement may also affect non-EU entities in certain circumstances.

EMIR distinguishes between two types of counterparties, financial counterparties (“FCs”) and non financial counterparties (“NFCs”). Broadly, FCs comprise EU- authorised investment firms, credit institutions, (re)insurance undertakings, UCITS or UCITS managers, certain institutions for occupational retirement provision and alternative investment funds (“AIFs”) managed by an EU-authorised or registered alternative investment fund manager. The Clearing Requirement, Risk Mitigation Requirement and Reporting Requirement apply to FCs.

An NFC is any in-scope entity for EMIR purposes other than a CCP or an FC. NFCs are sub-divided into two categories; namely, an NFC+ and an NFC-, depending on whether the relevant NFC meets certain clearing thresholds. An NFC+ is subject to broadly the same obligations as an FC, namely the Clearing Requirement, the Risk Mitigation Requirement and the Reporting Requirement. In contrast, an NFC- is only subject to the Reporting Requirement and the Risk Mitigation Requirement.

EMIR entered into force on 16 August 2012, however most of its requirements did not become immediately applicable and some, including the Clearing Requirement and margin requirements for uncleared derivatives (which form part of the Risk Mitigation Requirement) are currently being phased-in.

The EMIR Review

As is typical of EU financial services legislation, EMIR contains a review clause which requires the European Commission to review EMIR and prepare a general report for submission to the European Parliament and the Council. The Commission started its review in 2015 and submitted its report in November 2016. While the report indicated that there should be no fundamental changes to EMIR’s core requirements, it suggested a number of targeted amendments designed to simplify some of those requirements and remove disproportionate costs.

The Commission also included the EMIR review in its 2016 Regulatory Fitness and Performance programme (REFIT). The proposed Regulation follows on from the Commission’s report and the outcome of the REFIT evaluation.

The Proposed Regulation

The proposed Regulation will impact in particular on the definition of an FC as well as on the Clearing Requirement, Risk Mitigation Requirement and Reporting Requirement. The proposed Regulation will also impact on the rules applicable to CCPs and trade repositories.

You may access the proposed Regulation here.

Expanding the FC Definition

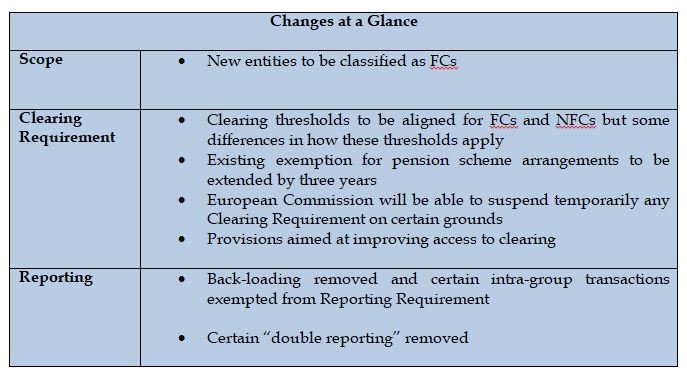

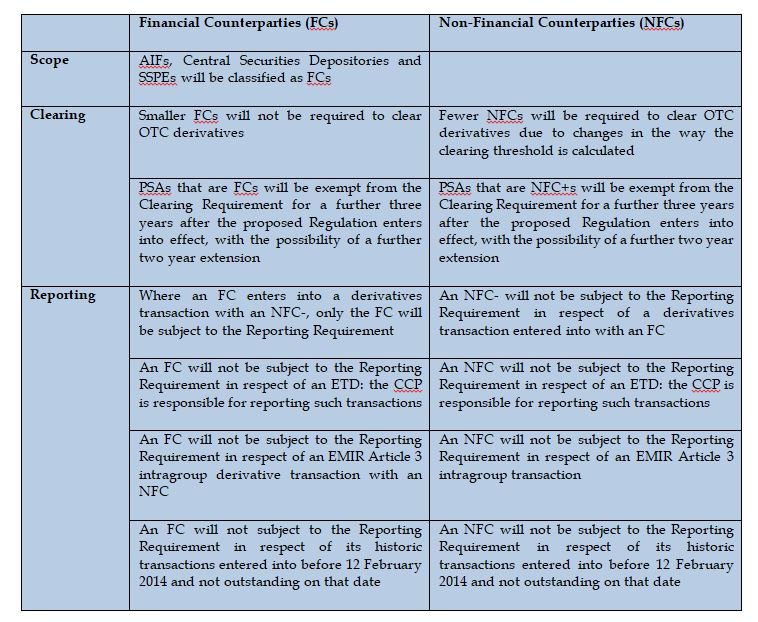

The proposed Regulation amends the definition of FC set out in EMIR to cover AIFs registered under national law, which are currently treated as NFCs. As a result a broader range of third country AIFs will be treated as third country entities that would be FCs if established in the European Union, for EMIR purposes. The proposed Regulation also extends the definition of FC to cover Central Securities Depositories and Securitisation Special Purpose Entities (“SSPEs”). This brings all SSPEs in scope for the Clearing Requirement (subject only to relief for those SSPEs that fall below the new clearing threshold for FCs) and the margin requirements of the Risk Mitigation Requirement.

Applying the margin requirement is likely to prove challenging for SSPEs that do not have access to liquid collateral assets: such SSPEs are likely to need to put in place liquidity, or other collateral transformation, facilities in order to margin their hedging arrangements. It is not currently proposed to apply any transitional provisions to this amendment.

Proposed Changes to EMIR Clearing

The proposed Regulation affects the Clearing Requirement as it applies to NFC+s, small FCs and PSAs. It also impacts on front loading for all FCs and NFC+s, and on incentives and access to clearing.

Furthermore, it provides for the suspension of the Clearing Requirement in certain circumstances.

Non-financial Counterparties (NFCs)

Under EMIR, an NFC becomes subject to the Clearing Requirement when the rolling average of its notional positions in OTC derivatives and those of other NFCs in its group exceed, over 30 working days, any of the clearing thresholds set by the Commission for a relevant class of derivatives. Once an NFC reaches the clearing threshold for any class of derivatives declared subject to the Clearing Requirement, it will have to clear derivatives in all such classes, even if it does not exceed the clearing thresholds for those other classes. Transactions entered into for hedging purposes do not count towards the clearing threshold.

The proposed Regulation changes the way the clearing threshold is calculated so that an NFC will become subject to the Clearing Requirement if its aggregate month-end average position for the months March, April and May exceed the clearing thresholds. This means that an NFC will have to assess the application of the Clearing Requirement once a year, rather than on a continuous basis, as is currently the case. Furthermore, under the proposed amendments, once an NFC exceeds the clearing threshold for a certain asset class, it will only become subject to the Clearing Requirement in respect of that asset class, rather than in respect of all asset classes. Transactions entered into for hedging purposes will continue to be excluded from the calculation of the clearing threshold.

The proposed change in the way in which the clearing threshold is calculated for NFCs will have significant operational implications for FC counterparties of entities that act as an NFC + in respect of some, and NFC- in respect of other, asset classes. Furthermore, it appears that an NFC that is treated as an NFC+ for the purpose of the Clearing Requirement for certain asset classes but an NFC- in respect of others may be treated as an NFC+ for all purposes other than the Clearing Requirement (eg, the margining aspects of the Risk Mitigation Requirement). The amendment is therefore of limited benefit.

Financial Counterparties (FCs)

Currently all FCs are subject to the Clearing Requirement although its application to smaller FC’s has recently been delayed until 21 June 2019 (see our briefing here). The delay applies to FCs that are:

- not clearing members of a Central Counterparty (CCP) in respect of at least one of the clearing classes, and

- belong to a group whose aggregate month-end average of outstanding gross notional amount of non-centrally cleared derivatives for the relevant assessment period is below €8 billion.

Under the Proposed Regulation, smaller FCs that do not meet the clearing thresholds applicable to NFCs will be exempt from the Clearing Requirement. These thresholds are, in gross notional value, €1 billion for credit and equity derivatives contracts; and €3 billion for interest rate, FX, commodity and other OTC derivative contracts.

While the Proposed Regulation applies the same clearing thresholds to FCs and NFCs for the purpose of the Clearing Requirement, there are some differences in the way this threshold applies. Specifically, FCs will be required to clear all OTC derivatives that are in-scope of the Clearing Requirement once they exceed the relevant clearing threshold for any asset class, in contrast to the proposed treatment for NFCs. Also, unlike the position for NFCs, an FC’s hedging transactions will be included in determining whether it has reached the clearing threshold and FCs will be fully subject to the Risk Mitigation Requirement, including the margining requirements, regardless of whether they meet the threshold.

Pension Scheme Arrangements

PSAs currently benefit from an exemption from the Clearing Requirement, pending the development of a viable technical solution for the transfer by PSAs of non-cash collateral as variation margin. This exemption will expire on 16 August 2018. The proposed Regulation extends the exemption for PSAs by a further three years. It also gives the Commission the power to extend the exemption once by two years by means of a delegated act.

There are concerns regarding whether the proposed Regulation will be in effect when the current exemption expires in August 2018: it may be necessary to amend the existing Delegated Regulation,2 which specifies the date the Clearing Requirement applies to PSAs to address this.

Front-loading

EMIR applies the Clearing Requirement to certain OTC derivative contracts entered into or novated before the date the Clearing Requirement takes effect, known as “front-loading”. Recognising that this “creates legal uncertainty and operational complications for limited benefits” the proposed Regulation removes this requirement.

Incentives and access

The proposed Regulation seeks to improve access to clearing by requiring clearing members and their clients who provide clearing services to other counterparties or offer their client the possibility to provide such services, to do so under fair, reasonable and non-discriminatory commercial terms (‘FRAND’ principle). Currently the standard required of a clearing member under EMIR is “reasonable commercial terms”. The Commission will be empowered to adopt a delegated act specifying the conditions under which the FRAND principle will be considered to be satisfied.

The proposed Regulation also clarifies that assets and positions recorded in the separate accounts maintained by a CCP for a clearing member or by a clearing member for its clients, under Article 39 of EMIR, are not part of the insolvency estate of the CCP or clearing member. Further consideration of the interaction of this principle with applicable insolvency laws (particularly those of non-EU member states) will be required.

CCPs will also be required to provide to clearing members a simulation tool allowing them to calculate the amount (on a group basis) of additional initial margin required for new transactions and information on their initial margin models. Clearing members have long sought additional transparency on CCP’s margin models particularly in light of clearing members’ liabilities in applicable default management processes. However, there are concerns that the new requirements do not go far enough, as the results generated by a CCP’s simulation tool will not be binding on the CCP. In turn, CCPs are concerned that the provision of more detailed information will enable clearing members to “game” a CCP’s risk mitigation system.

Suspension

The proposed Regulation gives the Commission the power to suspend temporarily any Clearing Requirement, on specific grounds, namely where:

- the criteria on the basis of which a specific class of OTC derivative has been made subject to the Clearing Requirement are no longer met – this could arise, eg where a class of OTC derivative becomes unsuitable for mandatory central clearing or where there has been a material change to one of those criteria in respect of a particular class of OTC derivatives;

- a CCP ceases to offer a clearing service for a specific class of OTC derivative or a specific type of counterparty and other CCPs cannot step in fast enough to take over the clearing services;

- suspension is deemed necessary to avoid a serious threat to financial stability in the EU.

Risk-mitigation Techniques

The proposed Regulation mandates the European Supervisory Authorities (“ESAs”) to develop draft regulatory technical standards in order to specify the supervisory procedures for ensuring initial and ongoing validation of risk- management procedures requiring the timely, accurate and appropriately segregated exchange of collateral, which risk-management procedures are currently required to be, and are, subject to such standards.

Reporting

One of the biggest complaints about EMIR is the structuring of the Reporting Requirement as double-sided reporting, meaning that both sides of an OTC or exchange traded derivative must report the trade. The proposed Regulation will eliminate the “double” Reporting Requirement for certain counterparties, require CCPs to report exchange-traded derivative contracts (“ETDs”), eliminate the Reporting Requirement for certain intragroup transactions, clarify who is responsible for reporting in specific circumstances and eliminate the Reporting Requirement in respect of certain historic transactions.

- Single-sided Reporting: an FC will have the responsibility, including any legal liability, to report a transaction between an FC and an NFC- on behalf of both counterparties;

- Exchange-Traded Derivatives: the CCP will have the responsibility, including any legal liability, to report an ETD on behalf of both counterparties as well as ensuring the accuracy of details reported;

- Intragroup transactions: intragroup transactions, within the meaning of EMIR Article 3, will no longer have to be reported where at least one of the two counterparties is an NFC;

- Historic transactions: counterparties will no longer be required to report their derivative contracts which were entered into before 12 February 2014 and were not outstanding on that date. Under the current rules, historic transactions must be reported by 12 February 2019.

The proposed Regulation does not provide for the phase-in of these changes and affected FCs and CCPs will need to ensure that they are ready to comply as soon as the amendments take effect. This may involve amending documentation and/or system adjustments.

Trade Repositories

The proposed Regulation also impacts on trade repositories relating to their registration, supervision, data quality, data availability and sanctions.

Next Steps

The proposed Regulation must now be considered by the European Parliament and by the Council and will enter into force 20 days after it is published in the Official Journal. The amendments to EMIR will apply within 6 or 18 months after that date, depending on the relevant amendment. The table below outlines the main changes for FCs and NFCs.

You may access the proposed Regulation here.

- Regulation (EU) No 648/2012 of the European Parliament and of the Council of 4 July 2012 on OTC derivatives, central counterparties and trade repositories.

- Commission Delegated Regulation (EU) 2017/610 of 20 December 2016 amending Regulation (EU) No 648/2012 of the European Parliament and of the Council as regards the extension of the transitional periods related to pension scheme arrangements, OJ L86/3, 31 March 2017.

This content has been prepared by McCann FitzGerald LLP for general guidance only and should not be regarded as a substitute for professional advice. Such advice should always be taken before acting on any of the matters discussed.

Select how you would like to share using the options below