New Regulatory Framework for the Cross-border Distribution of Investment Funds

The EU’s new regulatory framework facilitating the cross-border distribution of collective investment undertakings was published in the EU’s Official Journal on 12 July 2019. The new framework, which is intended to provide clarity for fund managers that want to market their products across the EU comprises:

- Regulation 2019/1156 on facilitating cross-border distribution of collective investment undertakings and amending the EUVECA Regulation 345/2013, the EUSEF Regulation 346/2013 and the PRIIPs Regulation 1286/2014 (the “Regulation”) (here); and

- Directive 2019/1160 which amends the UCITS Directive 2009/65 and the Alternative Investment Fund Managers Directive 2011/61 (“AIFMD”) in certain respects (the “Directive”) (here).

Overview

The new regulatory framework forms part of the European Commission’s (the “Commission”) goal to develop a Capital Markets Union in order to mobilise capital in the EU. It aims at promoting the cross-border distribution of investment funds by improving transparency and removing inefficiencies, thereby reducing costs for cross-border distribution and making it simpler, quicker and cheaper.

According to the Commission, in a press release dated 5 February 2019, only 37% of UCITS and about 3% of alternative investment funds (“AIFs”) are registered for distribution in more than 3 Member States. Moreover, over 70% of the total assets under management were held by investment funds authorised or registered for distribution only in their domestic market.

The main changes introduced by the new rules include amendments to the UCITS Directive and AIFMD, which are intended to:

- make it easier for EU AIF managers (“AIFMs”) to test the appetite of potential professional investors in new markets (so-called ‘pre-marketing’);

- clarify customer service obligations for asset managers in their host Member State;

- align procedures and conditions for managers of collective investment funds to exit national markets when they decide to terminate the offering or placement of their funds (so-called ‘de-notification procedure’);

- introduce increased transparency and create a single online access point for information on national rules related to marketing requirements and applicable fees.

The new regulatory framework is expected to result in substantial savings for funds marketed on a cross-border basis. According to the Commission:

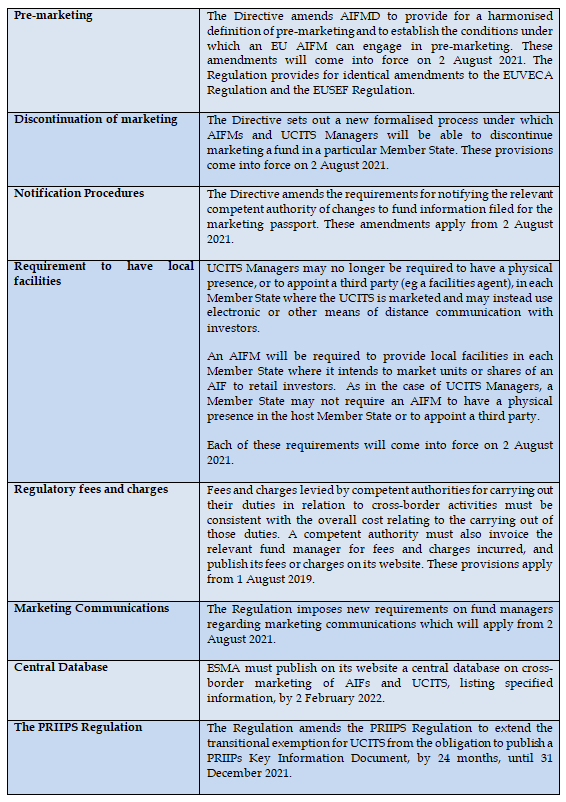

The Main Changes

The Table below sets out the key changes included in the new regulatory framework:

This content has been prepared by McCann FitzGerald LLP for general guidance only and should not be regarded as a substitute for professional advice. Such advice should always be taken before acting on any of the matters discussed.

Select how you would like to share using the options below