COVID-19: Central Bank of Ireland Announces Flexibility Measures for Funds, Fund Service Providers and Investment Firms

The Central Bank of Ireland (the “CBI”) has announced that funds, fund service providers1 (“FSPs”) and investment firms are to be allowed flexibility in respect of the remittance dates of a number of regulatory returns. This flexibility also extends to the submission of assurance reports regarding arrangements for the safeguarding of client assets or investor money and to the remittance dates for investment funds’ financial statements.

Overview

In recognition of the challenges facing firms and market participants due to COVID-19, the CBI, in a communication published on 16 April 2020 (the “Communication”) (here):

- stated that it is allowing flexibility in respect of the remittance dates of a number of regulatory returns due from investment firms, FSPs and investment funds over the COVID-19 period;

- clarified its expectations as regards the deadlines for the submission of assurance reports in respect of investment firms’ and FSPs’ arrangements for the safeguarding of client assets or investor money;

- clarified its expectations in relation to remittance dates for financial statements of investment funds;

- clarified its expectations regarding risk mitigation programme (RMP) implementation dates;

- stated that it is postponing its regular assessments of the domestic regulatory policy framework in respect of securities markets, investment management activities and investment firms; and

- confirmed that it will apply a number of measures outlined in recent announcements by ESMA.

Remittance Date Flexibility

The CBI will allow flexibility as regards the deadlines for the submission of the Return Types listed in Table A of the Communication, provided that the relevant investment firm or FSP submits the relevant return within the time frame listed in the “Extension Period” column of Table A.

Broadly, Table A provides as follows:

- Annual Audited Accounts – 2 month extension for submissions falling due from April to July 2020 inclusive;

- Capital Adequacy Returns – 1 month extension for reporting dates March to May 2020; and

- Management Interim Accounts – 1 month extension for reporting dates March to May 2020.

All reports and returns not listed in Table A or dealt with elsewhere in the Communication must be submitted in accordance with legislative requirements.

Client Asset and Investor Money Requirements

Regulations 68(4) and 83(3) of the Central Bank (Supervision and Enforcement) Act 2013 (Section 48(1)) (Investment Firms) Regulations 2017 (the “Investment Firm Regulations”), set out deadlines for the submission of assurance reports in respect of investment firms’ and FSPs’ arrangements for the safeguarding of client assets or investor money.

For submissions falling due from April to July 2020 inclusive, where it is not possible to comply with those deadlines as a result of COVID-19 related issues, the relevant assurance report may be submitted within an extended two months from the date on which the reporting obligation falls due. However, an investment firm or FSP that is relying on this extension must notify their usual contact on the Client Asset Specialist Team (CAST) or contact the CAST mailbox (CAST@centralbank.ie) in a timely manner, explaining the rationale for relying on the extension and, to the extent possible, the estimated submission date.

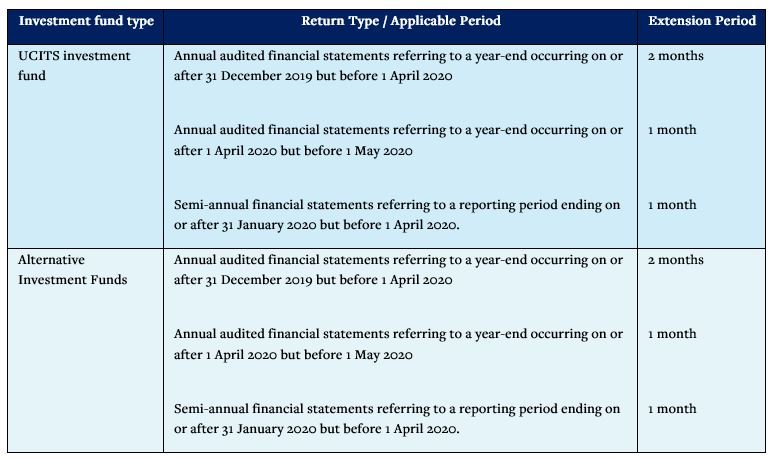

Remittance Dates for Financial Statements for Investment Funds

The CBI will allow flexibility if an authorised investment fund is unable to file its financial statements with the CBI within the usual time frames, as listed in Table B of the Communication (see below), provided that the authorised investment fund (or its management company or AIFM in respect of the investment funds managed by it):

- promptly notifies the CBI and informs investors as soon as practicable of the delay, the reasons for such a delay and to the extent possible the estimated publication date; and

- submits the relevant regulatory return within the timeframe listed in the “Extension Period” column in Table B below.

Table B

Risk Mitigation Programmes (RMPs)

Individual firms can engage directly with their usual supervisors where they have difficulties in relation to meeting specific RMP submission dates and those supervisors will consider on a case-by-case basis whether the postponement of such measures may be consistent with the objectives set out in the Communication.

Updates to CBI Regulatory Policy Frameworks

As part of wider efforts to ensure that firms can navigate the current market dynamics, the CBI will delay updates to its domestic regulatory policy frameworks in respect of investment firms, FSPs and investment funds. The CBI will also delay the publication of its feedback statement arising from Consultation Paper 130 (CP130), Treatment, Correction and Redress of Errors in Investment Funds. Further updates will be provided on the expected publications in respect of each area in due course.

ESMA

The CBI will apply the measures as outlined in recent announcements by ESMA regarding:

- Securities Financing Transaction Reporting (19 March 2020);

- MiFID II requirements on the recording of telephone conversations (20 March 2020);

- the new tick size regime for systematic internalisers (20 March 2020);

- publication deadlines under the Transparency Directive (27 March 2020) - where issuers reasonably anticipate that publication of their financial reports will be delayed beyond the deadline set out in the Transparency (Directive 2004/109/EC) Regulations 2007, they should inform the CBI by email to regulateddisclosures@centralbank.ie and, in accordance with the ESMA statement, disclose to the market that publication will be delayed, the reasons for such delay and, to the extent possible, the estimated publication date;

- publication of the general best execution reports under MiFID II (31 March 2020);

- Money Market Fund managers quarterly reporting (31 March 2020); and

- publication of investment funds periodic reports (9 April 2020).

See our previous briefings here and here.

- Including (i) management companies authorised pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations 2011, (ii) alternative investment fund managers and AIF management companies authorised (or registered, where relevant in the case of AIFMs) pursuant to the European Union (Alternative Investment Fund Managers) Regulations 2013 and (iii) depositaries.

This content has been prepared by McCann FitzGerald LLP for general guidance only and should not be regarded as a substitute for professional advice. Such advice should always be taken before acting on any of the matters discussed.

Select how you would like to share using the options below